What is a SSRPS™… What is a Safely Structured Retirement Planning Strategy?

A Safely Structured Retirement Planning Strategy™/SSRPS™ can be considered a “Modern Financial Planning Discipline”, an approach used in retirement planning, and/ or estate planning, and/ or special needs planning.

In utilizing a SSRPS™, a consumer with the help of their financial professional, structures their assets (or a portion there of), using “insured/ guaranteed financial/ retirement products*”, a particular type of annuity, and/ or particular life insurance contracts, to protect and grow assets, and/or to protect and grow income streams.

When a person has a SSRPS™ their a) principal is protected, b) any gains/ interest earned is locked-in/ protected from future market/ index downturns and c) they never run out of money/ income in retirement. * In addition, a SSRPS™ will d) eliminate inflation risk, to the degree by which the consumer receives a contractually guaranteed increasing income stream*. In fact, the income stream generated from a SSRPS™ will potentially far outpace inflation. You will learn there are also benefits with respect to e) the ability of a SSRPS™ income stream to cover a substantial amount of any cost related to a future medical crisis, where an individual cannot perform 2 of 6 activities of daily living, or they have Alzheimer's, where an individual may need home health care, or private nursing, or assisted living, or long term care, and there is no medical underwriting with the annuity side of SSRPS™. A SSRPS™ can do even more than bringing financial health to a client's retirement planning strategy, as there are f) health and wellness benefits associated with having a stress-free retirement income stream. You will immediately become familiar with g) what we call a "Spendable Income Advantage" that a SSRPS™ has over other planning strategies, which utilize traditional investments alone or predominantly.

How much Money/Retirement Income can I get with SSRPS™?

A SSRPS™ can readily generate substantially more money than what you put into it, over time, meaning depending on your age, you could receive 2, 3, 4, 5, 10, 20 times more money than what you have in your retirement accounts, savings accounts, or investment accounts today. A SSRPS™ can serve as a Personal Pension ensuring that when you retire you will have income for the rest of your life regardless of what is going on in the economy or the stock market. With a SSRPS™ you have contractual protection of your principal (the money you put in), contractual protection of any growth/ credited interest, contractual protection of your guaranteed lifetime income that will increase over time. A SSRPS™ alone can accomplish all of this, because a SSRPS™ truly is a unique planning strategy. A SSRPS™ is again a Modern Financial Planning Discipline, a fusion of investment and administrative efficiencies and actuarial pooling principals, where consumers can benefit from a combination of contractual guarantees plus product performance.

Can You Provide a High Level but Simple View of SSRPS™ & Equivalent Wealth?

- You are either going to need to earn a rather steady/high compounded single digit rate of return/interest rate for THE REST OF YOUR LIFE or

- You are going to need to start off with a lot more money

- If a conservative person is happy earning 4% with a CD at the bank, so they would need to put $2,121,983 into that 4% CD, in order that they could begin at age 65 to pull out the same income stream as our SSRPS™; totaling $3,311,317 through age 87 and $4,828,478 through age 92 . This example required 121% more money to receive the same retirement income as our SSRPS™.

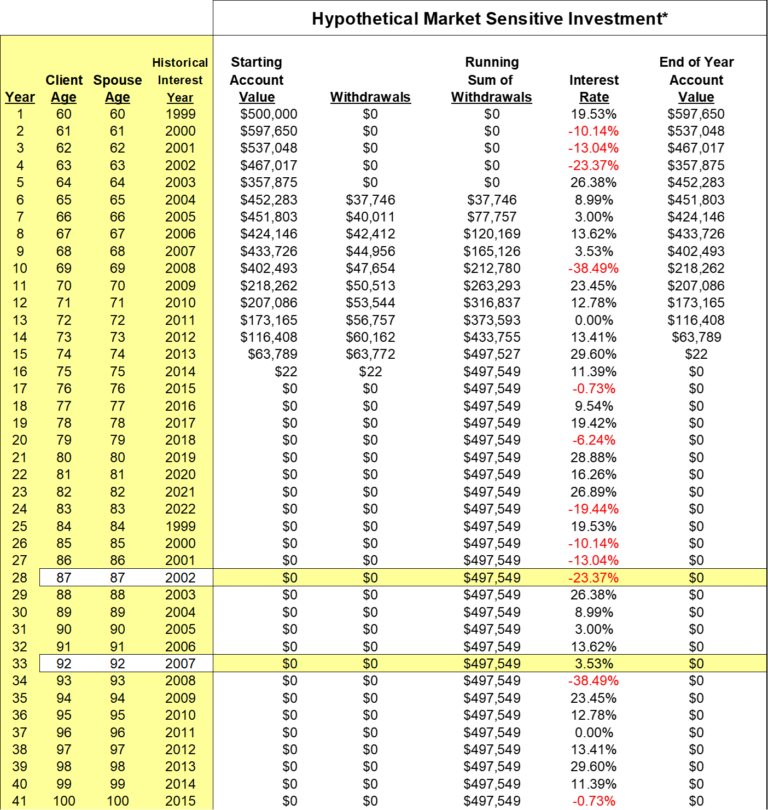

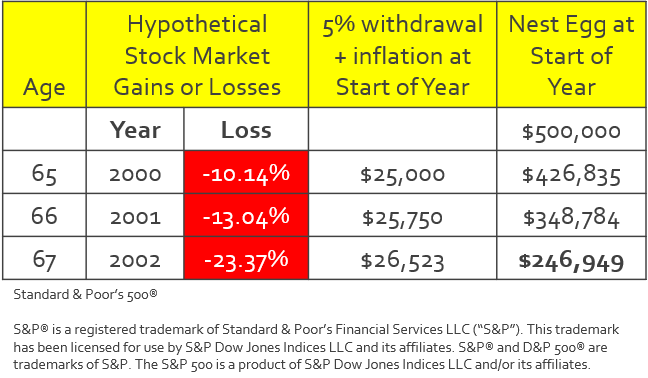

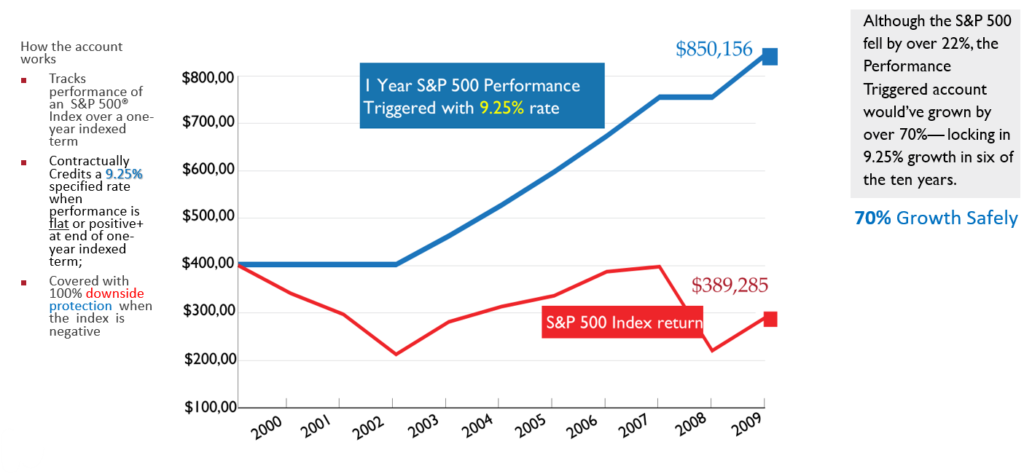

- A person who is willing to accept risk put’s his or her money into the stock market on January 1st 1996, where the 1st 4 years of returns represents an “Example of significant positive returns in the early years” relative to Sequence of Return Risk which were 20.26%, 31.01%, 26.67%, and 19.53%, and this person would need to put in $1,262,020, in order that they could begin at age 67 to pull out the same income stream as our SSRPS™, totaling $3,311,317 through age 87 and $4,828,478 through age 92. This example required $1,262,020, or 26% more money to receive the same retirement income as our SSRPS™.

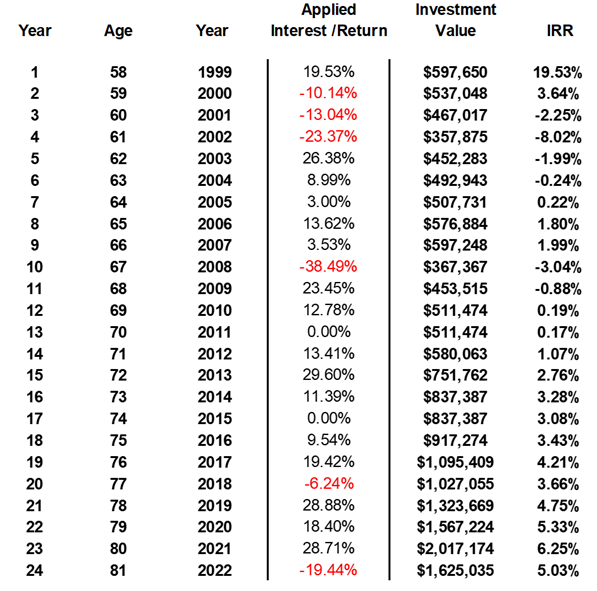

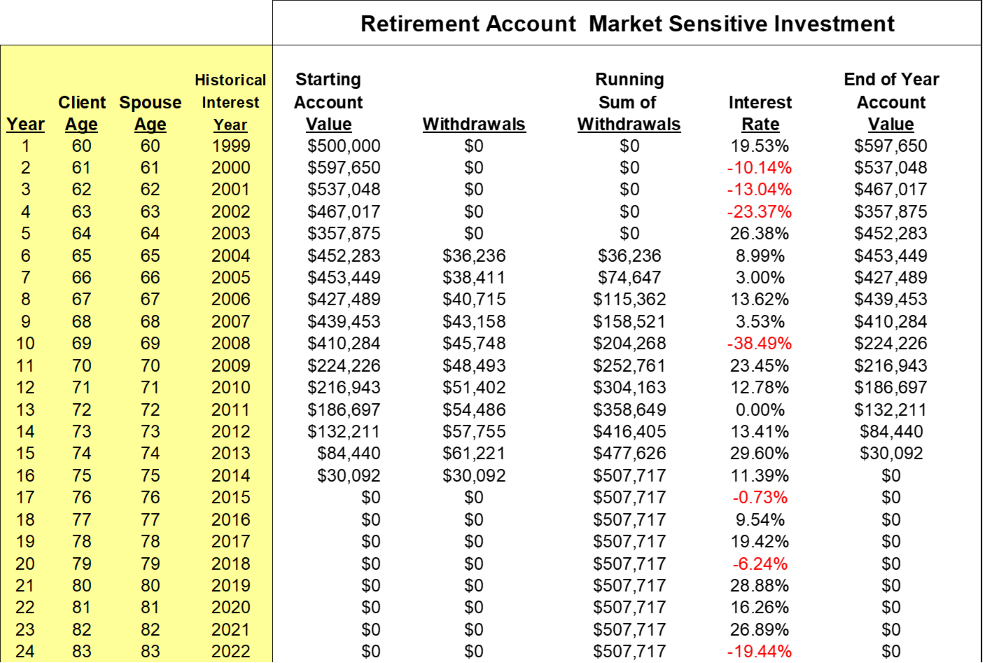

- A person who is willing to accept risk put’s his or her money into the stock market on January 1st 1999, where the 1st 4 years of returns represents an “Example of significant negative returns in the early years” relative to Sequence of Return Risk which were 19.53%, -10.14%, -13.04%, and -23.37%, and this person would need to put in $2,405,224, in order that they could begin at age 67 to pull out the same income stream as our SSRPS™ totaling $3,311,317 through age 87 and $4,828,478 through age 92. This example required $2,405,224, or 140% more money to receive the same retirement income as our SSRPS™.

Is SSRPS™ like a pension?

Consider that a SSRPS™ is technically not a pension, but a SSRPS™ will contractually serve as a Personal Pension. And just as folks have referred to a pension as a “paycheck for life”, so too can a SSRPS™ provide you with a “paycheck for life”. In fact a SSRPS™ can ensure, or shall we say insure, that you will have guaranteed income that increases over time for the rest of your life regardless of what is going on in the economy or the stock market.

Is my principal and interest safe with a SSRPS™?

With a SSRPS™ your principal, plus any growth/interest, along with your guaranteed lifetime income are protected, and guaranteed against loss; you cannot lose a dime.

Will the income from a SSPRS™ Keep-up with inflation?

The SSRPS™ guaranteed lifetime income will increase over time based on a) only positive movements in a stock market index, and/ or b) based on a fixed interest rate, for example 4.5%.

How is it that the income from a SSRPS™ can be greater than the income derived from my investments in the stock market or the savings account or CD that I have at a bank?

A SSRPS™ alone can accomplish all of this, because a SSRPS™ is truly a unique planning strategy. A SSRPS™ is in fact a Modern Financial Planning Discipline, where there is a fusion of investment, administrative and actuarial efficiencies, where consumers benefit from a combination of contractual guarantees plus product performance, where a person or persons can receive contractually guaranteed increasing income for the rest of their life, regardless of how long they live. Traditional investing or saving "has no actuarial support", or "there is no pooling advantage" associated with traditional investing or saving, so in retirement, when you take distributions/withdrawals from your savings/investments, your income will continue only for as long as your assets last. Consider that when you are retired, any money you have invested in the stock market will be subject to the ups and downs of the stock market/economy, meaning sometimes the value of your assets will increase and sometimes it will decrease, and then you have to account for the distributions/withdrawals you are taking. The point is, experiencing negative years early or too often can diminish the total value of your remaining assets. Over time, your withdrawals combined with such losses can chip away at your assets and cause your money to run out more quickly than anticipated. Consider using a "

SSRPS®

annuity" with a Type #2 income stream as part of a strategy to help you manage sequence-of-returns risks for your retirement income.

What Is The Spendable Income Advantage of SSRPS™ All About?

When you have a SSRPS™, “you genuinely have the opportunity to spend all of your money in a stress-free manner”. There is this “Spending Phenomenon” relative to having a Safely Structured Retirement Planning Strategy™, in that a person with a SSRPS™ has the potential to literally spend all of their money many times over, resulting in a “Spendable Income Advantage”. It can be demonstrated that a person with a SSRPS™ can afford to spend their money in a more “carefree manner”, where they can immediately begin to enjoy their retirement, where they can immediately spend more of their money than typical traditional planning may allow, and they can spend that money without concern of ever running out of money, because they enjoy guaranteed lifetime increasing income potential, contractually. Thus, a person with a SSRPS™ can enjoy stress-free spending in retirement, more so perhaps than a person with a more traditional retirement planning strategy, where their ability to spend money in retirement will be more closely tied to their retirement account values which fluctuate with the ups and downs of the stock market.

Why do you say that there are health and wellness benefits associated with SSRPS™ that are not associated with traditional saving or investing?

What are the new/ various opportunities that a SSRPS™ provides, that people may not otherwise have?

The guaranteed increasing income opportunity provided from the SSRPS™ income stream gives people new planning opportunities. Consider that people with a SSRPS™ income stream gives people new planning opportunities. Consider that people with a SSRPS™ can put a legacy plan in place, they can leave money to the heirs, without it being a financial burden, in a manner that just isn't possible when people rely on traditional wealth management alone, stocks and bonds and mutual funds etc...

How can a SSRPS™ act as a portfolio protection plan, thus protecting a person’s overall savings and investment portfolio/ wealth?

When a person has a SSRPS™, there are benefits relative to a person's other assets. Consider that if a person has a SSRPS™, but a person also has for example 50%/60%/70% of their overall investible wealth invested elsewhere, be it in the stock market, real estate, or other ventures...if they have a SSRPS™, then if/when the stock market takes a deep downturn, i.e. 20%, 30%, 40%, or even 50%, a person with a SSRPS™ may be in a position to "leave those other assets alone", or "not take as much money from such accounts" after a loss, which may allow those assets/ accounts to recover when the market turns upward again.

Has SSRPS™ changed the nature of Retirement Planning and Financial Planning?

The world of financial planning/ retirement planning/ estate planning/ special needs planning, has forever changed, it’s just that people don’t know what they don’t know.

People can now structure their assets differently than they had in the past and receive long term financial security that simply was never available, prior to the development/design of a "Type #2 Income Stream". The type #2 Income Stream allows people to literally, safely leverage their assets/money/savings/investments, to not only secure their financial future, but to perhaps make their retirement and legacy dreams come true.

The SSRPS™ platform / software provides an experiential learning opportunity for people to discover new planning opportunities.

Hence, I call SSRPS™ “a Modern Financial Planning Discipline”, a fusion of investment/ administrative and actuarial efficiencies.

When is it to early to start a SSRPS™?

It is never to early or too late to start a SSRPS™, as a SSRPS™ can be put together for children where the owner is a guardian, and they can be put together for an 80 year old (maximum age).

What happens to my money if I pass only a few years after putting our money into a SSRPS™ product?

The money that you put into a SSRPS™ is always protected, your principal is always protected against loss (principal is the money you put in), the interest is protected (any fixed interest or market-linked interest you earn is locked-in and protected), and your income is protected as well, your retirement income is guaranteed for as long as you or you and your spouse live, even if you live to be around 120.

So if you the "owner pass away", your account value or an enhanced account value can go directly to your beneficiary/heirs, however, if you are married, via "spousal continuation" your spouse can keep the contract and a) continue to receive the income stream or b) they can take the account value or an enhanced account value as a death benefit.

The point is, your money is safe and will pass on to loved ones one way or another.

What are the spousal benefits with a SSRPS™?

Understand that when you have a SSRPS™ and a spouse passes, the surviving spouse is financially protected, as he or she will never run out of "lifetime income" that continues to increase over the years for as long as they live.

What would happen if you were still alive and ran out of money...Would you go back to work? Would you move in with children? Would you have to cancel your retirement plans/goals, etc?

With a SSRPS™ you can never run out of money/income because a SSRPS™ will serve as a "Modern Personal Pension Plus"...providing long-term financial security with guaranteed lifetime income, that increases over the years via only positive stock market indexing interest credits, or by a fixed interest rate credit, to help you keep up with or outpace inflation.

Do I have to invest all my money into a SSRPS™?

Every situation is different so the amount of money someone many dedicate to a SSRPS™ depends on their particular situation.

What is the cost associated with setting up my Safely Structured Retirement Planning Strategy?

The financial professional is compensated directly from the company relative to the products associated with a SSRPS™, so there are no costs or fees that you will ever pay to the financial professional relative to the products associated with a SSRPS™.

Will you outlive your savings and run out of money?

Well not if you have a SSRPS™.

"Why?" or "How can you say that?"

When you a have SSRPS™, it means that your retirement plan is contractually guaranteed, it is "Stock Market Crash Proof" and "Recession Proof" and "Inflation Proof" and to a degree, "Medical Crisis Cost Proof"

When you have a SSRPS™, you have a contractually guaranteed income stream that will increase over the years, an income stream that will come to you or you and your spouse, for as long as either one of your lives, an income stream that will help you keep up with or even outpace inflation, an income stream that can help you pay for medical care related to "Home Health Care" or "Long-Term Care" or "Assisted Living" or "Private Nursing" or "Alzheimer's Care"

How is living longer a Risk Multiple?

Consider the reality that "Longevity" or "Living Longer" is a "Risk Multiplier".

Consider the reality that "Longevity" or "Living Longer" is a "Risk Multiplier".

- Longevity is a risk multiplier because as we live longer, the more likely we are to experience the ill effects of inflation, where we lose purchasing power over time. So we really need a reliable retirement income stream that can grow larger and larger over the years, in order that we can keep up with or even outpace inflation.

- Longevity is a risk multiplier because as we live longer, the more likely we are to experience stock market volatility, a recession, or an outright stock market crash.

- Longevity is a risk multiplier because as we live longer, the more likely we are to experience a medical crisis where we may need "Home Health Care" or "Long-Term Care" or "Assisted Living" or "Private Nursing" or "Alzheimer's Care".-Most people are concerned about the potential cost of "Home Health Care" or "Long-Term Care" or "Assisted Living" or "Private Nursing" or "Alzheimer's Care"...yet most people have no plan to cover such costs...(or no financial capability, so they think...)

Can a SSRPS™ eliminate my fear and worries about money and being able to retire comfortably?

I believe a SSRPS™ can eliminate your fears and your worries about being able to retire comfortably.

A comfortable retirement is part of the American dream, and although studies indicate that many people spend hours worrying everyday of their life about retirement and money, believing that “a comfortable retirement may be hard to reach”, you might say “that’s only because they don't know about SSRPS™”.

I can show you that if a person dedicates enough of their savings / wealth to a SSRPS™, that they could have more money coming to them in retirement, based on both performance and contractual guarantees, than perhaps they ever dreamed possible.

If you look at your assets, and you make SSRPS™ part of your overall plan to have a diversified retirement planning strategy, you will have a retirement planning structure in place, a safe structure; you will in fact have a Safely Structured Retirement Planning Strategy™.

If you take enough of your retirement savings and you put that money into the appropriate SSRPS™ insured financial products, you will then receive a guaranteed increasing income stream in retirement that will come to you or to you and your spouse for the rest of your life, and then you shouldn’t be worrying about running out of money.

Your SSRPS™ case design will show you what you should reasonably expect to receive, based on both performance and contractual guarantees, and that should make you feel much better, much more comfortable when you retire. Although many Americans feel they are unprepared, people who have a personal SSRPS™ designed just for them may be pleasantly surprised at the income they could reasonably expect to receive.

The real driver of retirement savings flowing into the Modern Financial Planning approach we call SSRPS™, is the confidence, the peace of mind, the joy, the excitement one will feel when they set up their SSRPS™. With a SSRPS™… you really can have a happy and healthy retirement.

Consider that “Millennial Americans worry 1.9 hours a day - 13 hours a week - 28 full days a year”, and people “ages 45 and up worry about money every day on average 1.6 hours a day – 11 hours a week – 24 full days a year”*. I contend that all or much of that worrying could disappear the moment they saw their personal SSRPS™ case design.

*Taken from a Schroders 2023 US RETIREMENT SURVEY, Retirement readiness report.

How can a SSRPS™ provide "Coverage" for Long-Term Care, Assisted Living, Home Health Care, Senior Living?

Consider that a SSRPS™ can contractually help in this regard, as a SSRPS™ through the guaranteed lifetime increasing income payments can help to pay for any costs related to a potential medical crisis.

A SSRPS™ can readily provide “coverage”… in that a SSRPS™ will help pay for medical care. Furthermore, the guaranteed lifetime increasing income payments can Double (provided the accumulation value is not exhausted), if either you or your spouse (with "joint income selected") can’t perform at least two of the six Activities of Daily Living (ADLs) and or if a person is confined to a qualified hospital for at least 90 days in a consecutive 120 day period, and in all states except California, if a person is confirmed to have severe cognitive impairment.

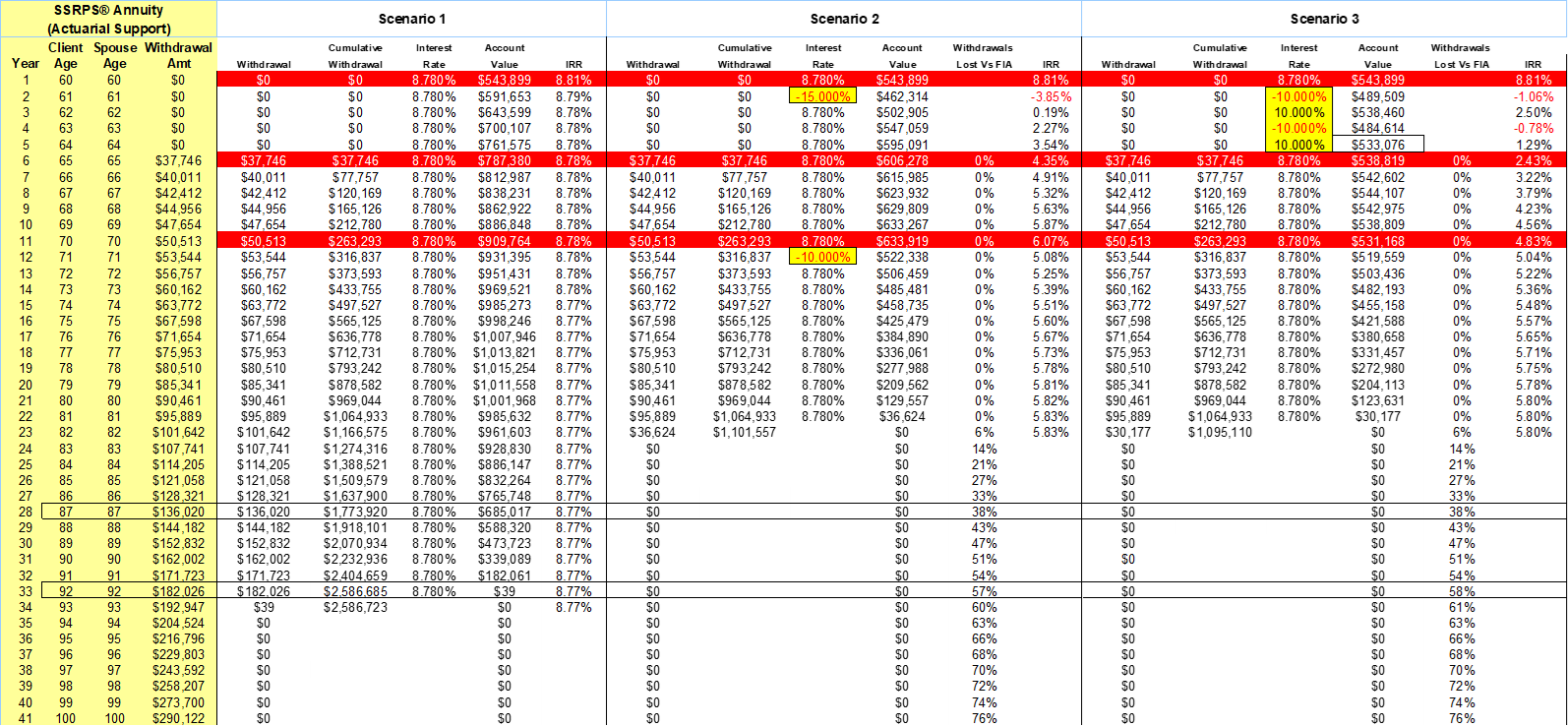

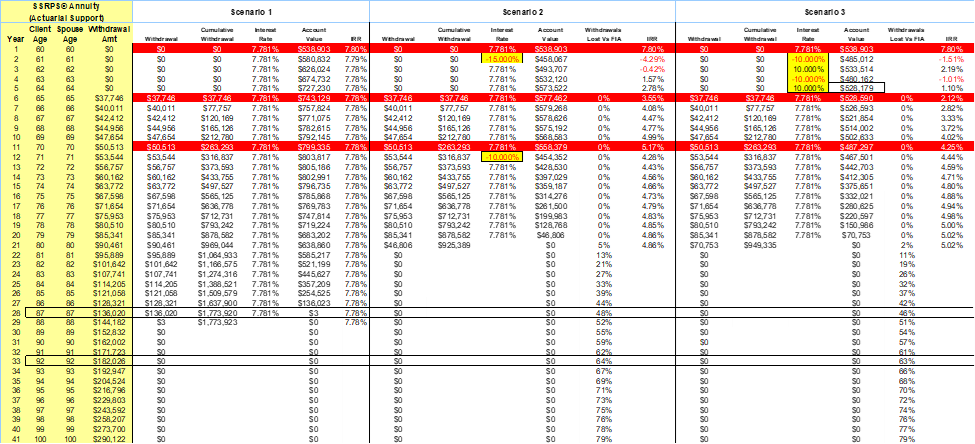

Also, consider that even if the accumulation value is exhausted, meaning your payments cannot Double any more, your guaranteed lifetime income payments can be quite substantial, where they have increased enough over time where the guaranteed lifetime income payments you or you and your spouse are receiving could help pay for any costs related to medical care. Hopefully your guaranteed lifetime income payments will help pay a substantial portion of any cost of care… for as long as you, or you and your spouse live. Through the 1st 19 years in our example on this website, the guaranteed income “could Double” because there is still money in the accumulation value, again a requirement for the “Doubling”. After that point, you have to consider that the guaranteed income (without any Doubling) has grown to be quite substantial. For example, remembering that our hypothetical 60 year old clients put $500,000 into a "SSRPS™ annuity", through age 82 they received $1,166,575 in payments, and that year they saw their payment hit $101,642, and at age 85 it was $121,058, and at age 87 it was $136,020, and at age 92 it was $182,026.

Understand that those guaranteed lifetime income payments can be used anyway you like, meaning that if you are healthy you can spend that money traveling the world or giving it away to children and grandchildren or your favorite charities, but if you need it for medical care it is there. Keep in mind there is no medical underwriting when it comes to having a SSRPS™. Also keep in mind that no one will ever tell you “what you can and can’t do with your money”, those guaranteed lifetime income payments are your’ s to do with as you please, they will get deposited into your checking account automatically (every month or quarter or every 6 months or even annually if you like), and that’s it… So no doctor, no caregiver, no insurance company will ever tell you what you may or may not use your guaranteed lifetime income payments for…

(The Activities of Daily Living (ADLs) are daily functions most adults can perform without assistance: eating, bathing, getting dressed, toileting, transferring, and continence. To be eligible via activities of daily living, a physician must certify that you are unable to perform at least two of the six ADLs. Diagnosis must occur during the contract year prior to beginning lifetime income withdrawals or any time thereafter.)